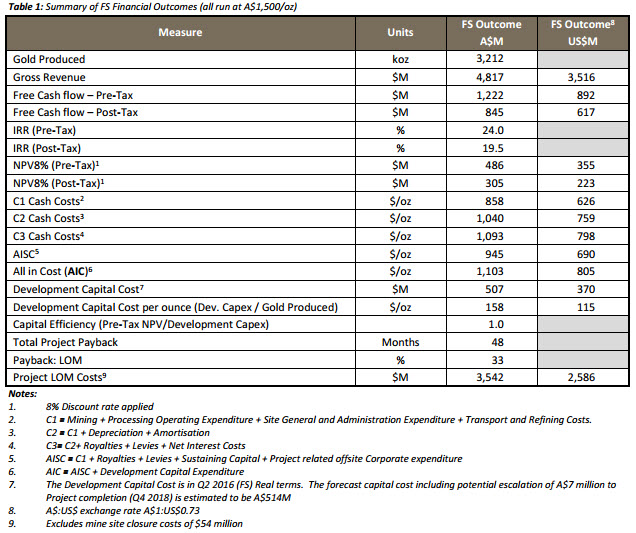

Gold Road has completed a positive Feasibility Study for the development of its 6.16 million ounce Gruyere Gold Project, located 200 kilometres east of Laverton in WA. The FS confirms an Ore Reserve in excess of 3.5 Moz over a 13-year Mine Life, and indicates a technically sound and financially viable project generating A$1.2 billion in free cash (pre-tax) over the Project life. The total forecast capital cost is estimated to be A$507 million.

Highlights

- Feasibility Study confirms Gruyere Gold Project as one of the longest life, lowest cost(1), undeveloped gold deposits in the world

- Updated Ore Reserve of 3.52 million ounces(2), supporting average annual gold production of 270,000 ounces over life-of-mine3 (LOM) of 13 years, elevating Gold Road into the ranks of Australia’s mid-tier gold producers

- Gruyere Open Pit averages more than 9,250 reserve ounces per vertical metre to a final depth of 380 metres

- Development to be based on a single large open-pit mine and conventional SAG/Ball Mill Circuit, gravity/carbon-in-leach plant with throughput of 7.5 Mtpa of fresh ore and up to 8.8 Mtpa of oxide ore

- Study findings indicate a technically sound and financially viable project generating in excess of A$1.2 billion in undiscounted free cash flow (pre-tax, at A$1,500 per ounce gold price) over an initial 15-year Project life(3)

- Total forecast capital cost of A$507 million(4),(5) (US$370 million(6)) with an additional A$77 million (US$56 million(6)) of sustaining capital over LOM

- Estimated average all-in sustaining cost (AISC) of A$945 (US$690(6))per ounce over LOM with a payback of less than one-third of LOM

- Net Present Value (pre-tax) (NPV8%(7)) of A$486 million (US$355 million(6)) and 24% Internal Rate of Return (pre-tax) (IRR) (at A$1,500 per ounce gold price)

- NPV8%(8) increases to A$910 million (US$664 million(6)) with 35% IRR at A$1,750 per ounce gold price

- Board approves Feasibility Study and progression to construction on completion of appropriate financing strategy

Gold Road Resources Limited (Gold Road or the Company) is pleased to announce the completion of the Feasibility Study (FS) for the development of its 6.16 million ounce8 (Moz) Gruyere Gold Project (the Project), located 200 kilometres east of Laverton in Western Australia. The FS confirms the Project as one of Australia’s most significant undeveloped gold deposits with an Ore Reserve in excess of 3.5 Moz over a 13-year Mine Life and a Project Life of 15 years.

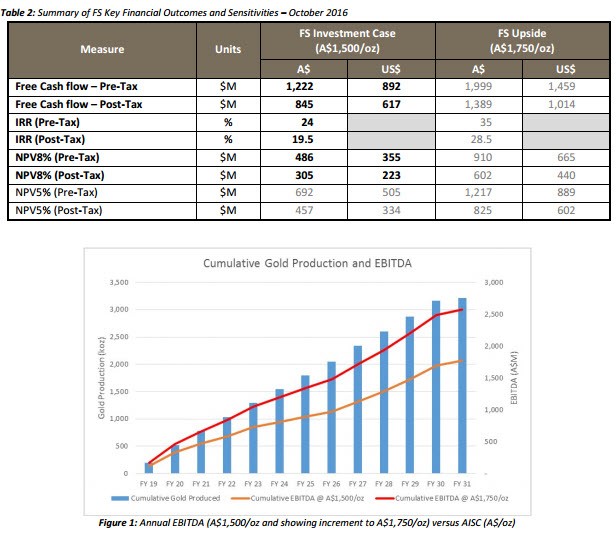

The FS indicates a technically sound and financially viable project generating over A$1.2 billion in free cash flow (pre-tax) over the Project life (Table 1). The total forecast capital cost is estimated to be A$507 million4,5 including a Project contingency of A$43 million. The FS is based on a pit design optimised at A$1,500 per ounce. All basecase financial analyses were completed assuming a A$1,500 per ounce gold price, representing the five-year historic average. Analysis at the more recent spot gold price (A$1,750 per ounce) demonstrates considerable project upside (Table 2 and Figure 1).

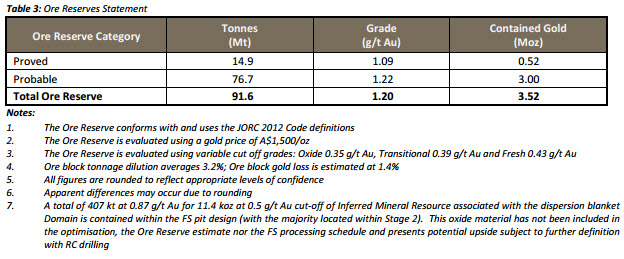

Completion of the positive FS allows the Company to declare an updated Ore Reserve for Gruyere of 3.52 Moz(9) , which supports an average annualised gold production of 270,000 ounces over the LOM. Production at this rate would elevate Gold Road into the ranks of Australia’s mid-tier gold producers.

Based on the positive FS outcome, the Gold Road Board has approved the FS and recommends progressing the Project to the construction phase pending successful completion of financing activities. The Company is in the final stages of assessing whether to opt for a combination of debt and equity arrangements or a Joint Venture with a third-party corporation. Project Finance discussions with a number of Australian and International Banking groups commenced in March 2016. The process is now well advanced and the Company is confident of receiving Credit Approved terms supporting a significant debt facility before the end of the year.

Parallel Joint Venture discussions have also been had with a select number of Australian and International gold mining companies since 2015. These talks are similarly well advanced and provide the Company with a number of potentially viable and attractive funding options.

Given the Company’s strong financial position10, the final financing decisions will be made at a time deemed most appropriate and beneficial to the Gold Road shareholder base.

The FS was compiled with the assistance of a number of independent, reputable and predominantly Western Australian-based engineering companies as well as other industry experts and qualified Gold Road personnel.

The FS has been evaluated at a A$1,500 per ounce gold price, representing the average price over the last five years. During the period of the FS the Australian dollar gold price traded between a low of A$1,592 to a high of A$1,83911 per ounce, at an average price of A$1,717 per ounce, with the price above A$1,700 for 65% of the FS period. The Project is highly leveraged to the gold price, as identified in Table 2 below which displays the potential financial performance at a gold price of A$1,750 per ounce. At this price, the Project generates an additional A$777 million (+63.6%) in pre-tax cash flows while the NPV almost doubles(+87.2%). Figure 1 also illustrates the potential uplift in EBITDA generated by a A$1,750 per ounce gold price compared to A$1,500 per ounce over the life of the Project. This price compares favourably with the Company’s existing modest hedging position of 50,000 ounces with a forward price of A$1,792 per ounce already secured for the Project.(12)

Ore Reserve(13)

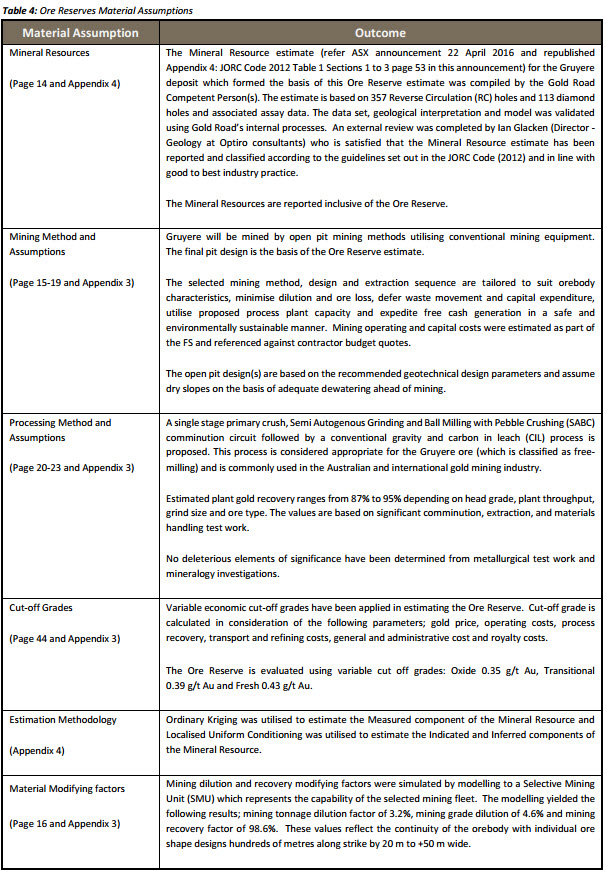

On the basis of the completed FS Gold Road has updated the Ore Reserve for the Project from the previous Ore Reserve announced on completion of the PFS14. Set out below is a summary of the key information material to understanding the reported Ore Reserve. A summary of the FS key information, including material information for the Ore Reserve, is provided in the body of this release. Additional details of the material assumptions are set out in Appendix 3 (JORC 2012 Table 1).

Gold Road intends to publish a full and complete Technical Report, being compiled by Behre Dolbear Australia (BDA), to complement the Feasibility Study. The BDA report will provide technical data on the FS and is planned to be released to the ASX within four weeks of this current release.

Overview of the Ore Reserve

The Ore Reserve for the Project was reported according to the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the JORC 2012 Code). The Ore Reserve was estimated from the Mineral Resource after consideration of the level of confidence in the Mineral Resource and taking account of material and relevant modifying factors. The Proved Ore Reserve estimate is based on Mineral Resource classified as Measured. The Probable Ore Reserve estimate is based on Mineral Resource classified as Indicated. No Inferred Mineral Resources have been included in the Ore Reserve.

Table 3 presents a summary of the Ore Reserves on a 100% Project basis at a A$1,500 per ounce gold price (US$1,095 per ounce at US$0.73:A$1.00).

Pursuant to ASX listing Rule 5.9.1, and in addition to the information contained in the body of this release and in Appendix 3 of this release, the Company provides the following summary (Table 4):

Commentary

Gold Road’s Managing Director and CEO, Ian Murray said: “Since the competion of the initial Scoping Study in 2015, a significant amount of work has been invested in the Gruyere Project Studies, culminating in this impressive Feasibility Study. The very thorough and high quality work delivered by the Owner’s team is self evident as is the economic strength of the Project, with its demonstrated low costs, strong cashflows and rapid payback. This has all been achieved at a World-leading Reserve discovery cost of less than A$10 per ounce.

While the Feasibility Study suggests a substantial Project life, the demonstrated exploration potential of Gruyere and the surrounding Yamarna region means that there is significant potential to extend the life beyond the current 15 years. Mineral Resources have previously been estimated for the Central Bore and Atilla-Alaric trends. None of this potential upside has been included in the scope of the Feasibility Study.

Again, we thank the Traditional Owners for their support in the work that we have undertaken on-country. We look forward to progressing the Gruyere Gold Project in a manner that cares for country and creates an enduring benefit for all involved.

We expect to be in a position to complete the funding aspects for the Project and make the associated investment decision in early 2017. It fills me with great pride to deliver, on behalf of our team, a 15-year Project within three years of its original discovery.”

(1) Australian Gold Miners – Australian equities in a global context – 10 October 2016, Macquarie Equities Research

(2) See Appendix 3: JORC Code 2012 Table 1 Section 4 page 44

(3) Project Life is duration from Construction to end of Processing. LOM is Mine Life duration of Mining and Processing for gold production

(4) Capital cost estimate is as at Q2 2016, and accuracy level is -10% to +15%

(5) Capital cost estimate includes A$43 million ($US31 million) of contingency, and excludes A$7 million escalation to Q4 2018

(6) A$:US$ exchange rate A$1:US$0.73

(7) 8% discount rate applied

(8) Gruyere Resource Increases to 6.2 Million Ounces (ASX announcement dated 22 April 2016)

(9) See Appendix 3: JORC Code 2012 Table 1 Section 4 page 44

(10) Cash on hand at 30 June 2016 of A$90 million

(11) A$ gold price as intraday bid asking price from Perth Mint records for the period 8 February to 30 September 2016

(12) Refer to ASX Announcement 1 September 2016

(13) See Appendix 3: JORC Code 2012 Table 1 Section 4 page 44

(14) Gruyere Pre-Feasibility Study Confirms Long Life Gold Mine (ASX announcement dated 8 February 2016)